Structural supply deficits persist through 2030 even

under aggressive supply expansion scenarios

Policy-driven demand visibility has strengthened

through legislative support for nuclear energy, reactor life

extensions, and small modular reactor requirements

Security-of-supply premiums are emerging as Western

utilities and governments prioritize supply chain

diversification

Operational leverage and cost curve positioning favor

companies with existing processing infrastructure,

restart-ready assets, or high-grade resource

endowments

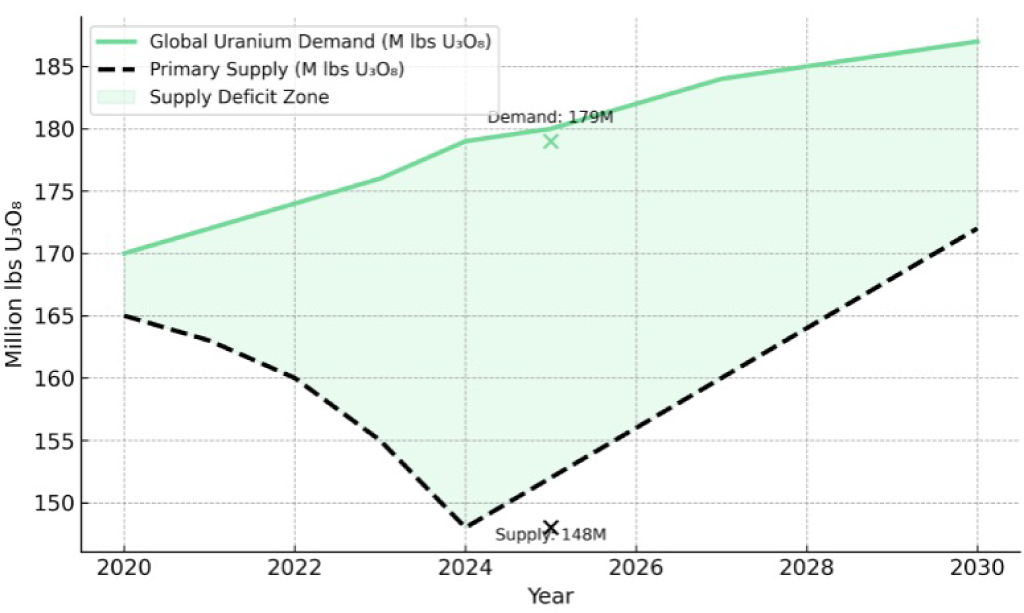

The structural case for uranium investment rests on supply-demand fundamentals that have materially improved and are projected to tighten further through the remainder of the decade

Click to enlarge

According to the World Nuclear Association’s 2025 Nuclear Fuel Report, global reactor requirements for 2025 are estimated at approximately 68,920 tonnes of uranium (equivalent to 179 million pounds U₃O₈),

Primary mine production is projected to reach approximately 140-150 million pounds annually. This creates an annual supply gap of roughly 30-40 million pounds

Uranium Supply

Supply Constraints, Geographic Concentration & the Security-of-Supply Premium

Click to enlarge

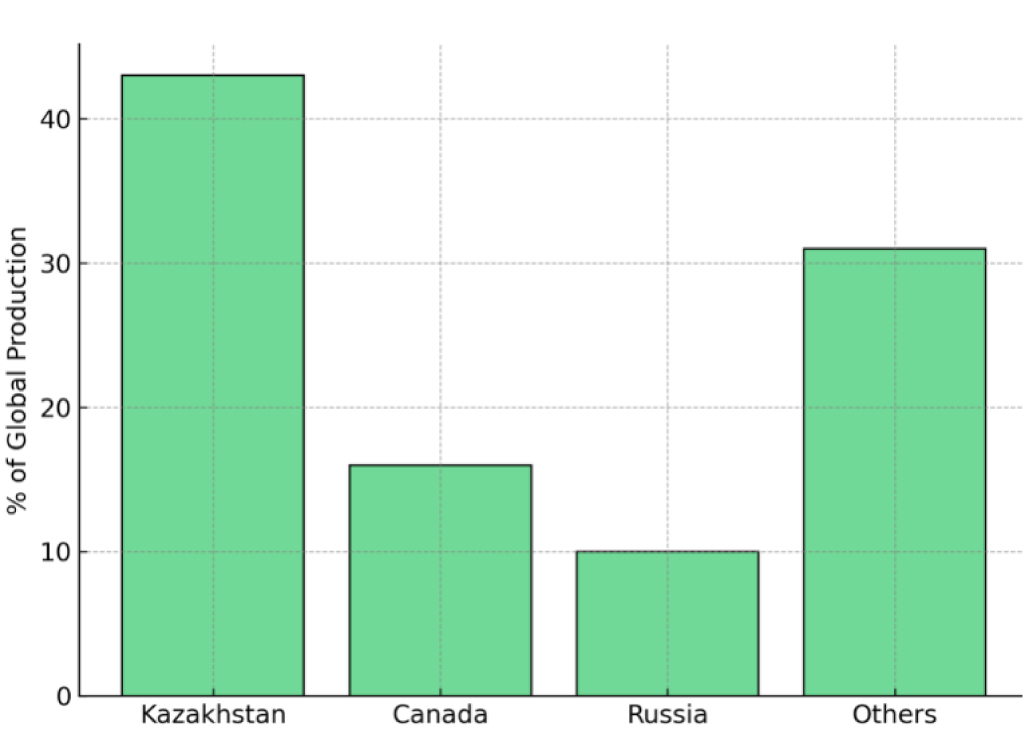

The uranium supply complex faces structural constraints that extend beyond simple production volume deficits. Geographic concentration represents a critical vulnerability, with Kazakhstan, Canada, and Russia collectively accounting for the majority of global primary production

Canada’s Strategic Importance

Canada was the world's largest uranium producer for many years, accounting for about 22% of world output, but in 2009 was overtaken by Kazakhstan.

With known uranium resources of 694,000 tonnes of U3O8 (588,500 tU), as well as much continuing exploration, Canada has a significant role in meeting future world demand.